Introduction

November brought a short-lived period of market volatility that impacted numerous asset classes. Although major indices have posted robust year-to-date gains across equities, fixed income, and international markets, concerns persist regarding artificial intelligence stocks and the Federal Reserve’s interest rate trajectory. Additionally, a government shutdown caused delays in releasing critical economic data, complicating efforts to assess the economy’s health.

By month’s end, many asset classes had stabilized and recovered from earlier declines. This pattern reinforces a crucial lesson for long-term investors: maintaining a well-balanced portfolio is essential for weathering market fluctuations. Effective investing demands commitment to long-term objectives rather than reacting to near-term performance shifts or news cycles.

What factors influenced November’s market activity and how should investors position themselvesheading into year end?

Notable Market and Economic Developments in November

- The S&P 500 increased 0.1% during November, while the Dow Jones Industrial Average

advanced 0.3% and the Nasdaq declined 1.5%. For the year through November, the S&P 500 has climbed 16.4%, the Dow has risen 12.2%, and the Nasdaq has surged 21.0%. - The VIX, which tracks stock market volatility, closed at 16.35 after reaching 26.42 during the month.

- The Bloomberg U.S. Aggregate Bond Index advanced 0.6% in November and has delivered a 7.5% year-to-date return. The 10-year Treasury yield concluded November at 4.02%, having temporarily dipped below 4%.

- International developed markets, measured by the MSCI EAFE Index, rose 0.5% in U.S. dollar terms, while emerging markets tracked by the MSCI EM Index fell 2.5%. Year-to-date gains stand at 24.3% for the MSCI EAFE Index and 27.1% for the MSCI EM Index.

- The U.S. dollar index finished November at 99.46, briefly surpassing the 100 threshold.

- Bitcoin dropped approximately 17% in November, closing at $91,176.

- Gold prices concluded the month at $4,218, remaining below October’s record high of $4,336.

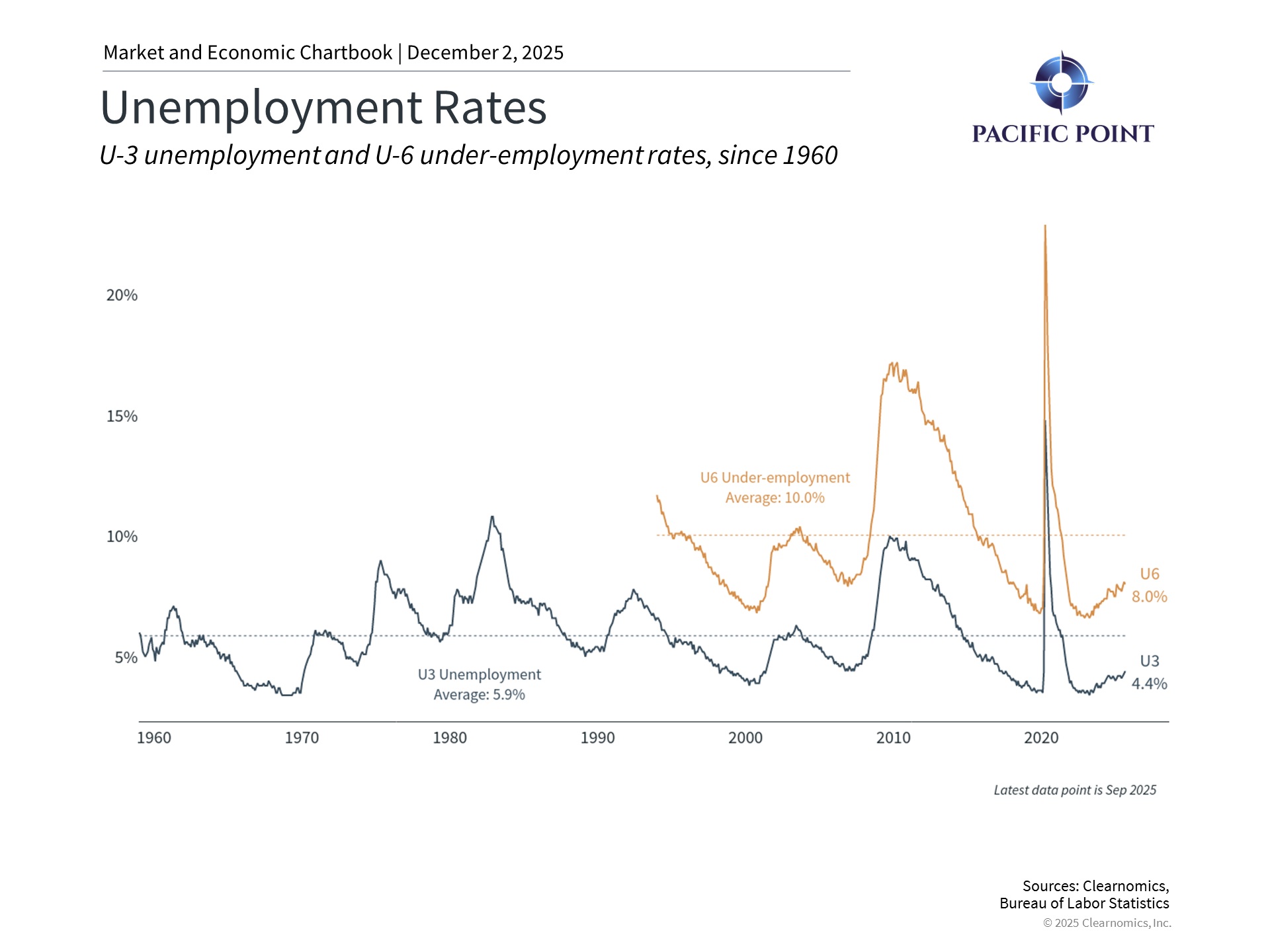

- The delayed September jobs report revealed 119,000 new jobs were created with the

unemployment rate increasing to 4.4%. No October jobs report will be issued.

Risk appetite temporarily declined across markets

Throughout November, investors temporarily shifted away from riskier assets including technology equities, highyield bonds, cryptocurrencies, and similar investments. This movement stemmed largely from doubts about the viability of AI-related investments and changing expectations regarding Federal Reserve rate reductions. The S&P 500 has experienced six pullbacks of 5% or greater this year, the highest count since 2022 though still near historical norms. Several major asset classes recovered in the month’s final days, with the S&P 500 finishing slightly positive.

AI-focused technology stocks endured their weakest week since April. Questions surrounding spending levels, debt obligations, profitability, and potential bubble conditions generated uncertainty. However, underlying business fundamentals remained solid, with companies like Nvidia posting strong third-quarter revenue and earnings results. Certain equities, including members of the Magnificent 7, rallied following these announcements.

Cryptocurrencies underwent a pronounced correction during this risk-averse period. Bitcoin

tumbled more than 30% from its early October peak above $125,000, briefly dropping below $85,000 and erasing its year-to-date appreciation. Despite increasing investor adoption of cryptocurrencies, such episodes highlight that these assets remain highly speculative and

vulnerable to dramatic swings. This reality emphasizes the continued importance of disciplined risk management and appropriate asset allocation.

Bond markets advanced in November, supported partly by declining long-term interest rates as the 10-year Treasury yield temporarily fell below 4% again. This decline reflected revised expectations about government policy that could produce lower rates over time. The Bloomberg U.S. Aggregate Bond Index has delivered a 7.5% year-to-date gain, its strongest performance since 2020, helping to provide stability within diversified portfolios.

Government shutdown concluded but economic visibility remains limited

The historic 43-day government shutdown has ended, though federal funding only extends through January 2026. This limited timeframe means political uncertainty will resurface in the coming months. Nevertheless, markets largely overlooked the shutdown, despite challenges created by missing economic data.

The Bureau of Labor Statistics published the delayed September jobs report, originally scheduled for October release. This data showed employment gains exceeded forecasts for that month, recovering from summer weakness. However, revised figures indicate 4,000

jobs were eliminated in August, marking the second month of negative employment growth this year. September’s unemployment rate edged up to 4.4%, the highest level since October 2021, though this remains low historically.

A complete October jobs report will not be available since household and business surveys were suspended during that month, although some October data will appear in November’s report on a delayed schedule.

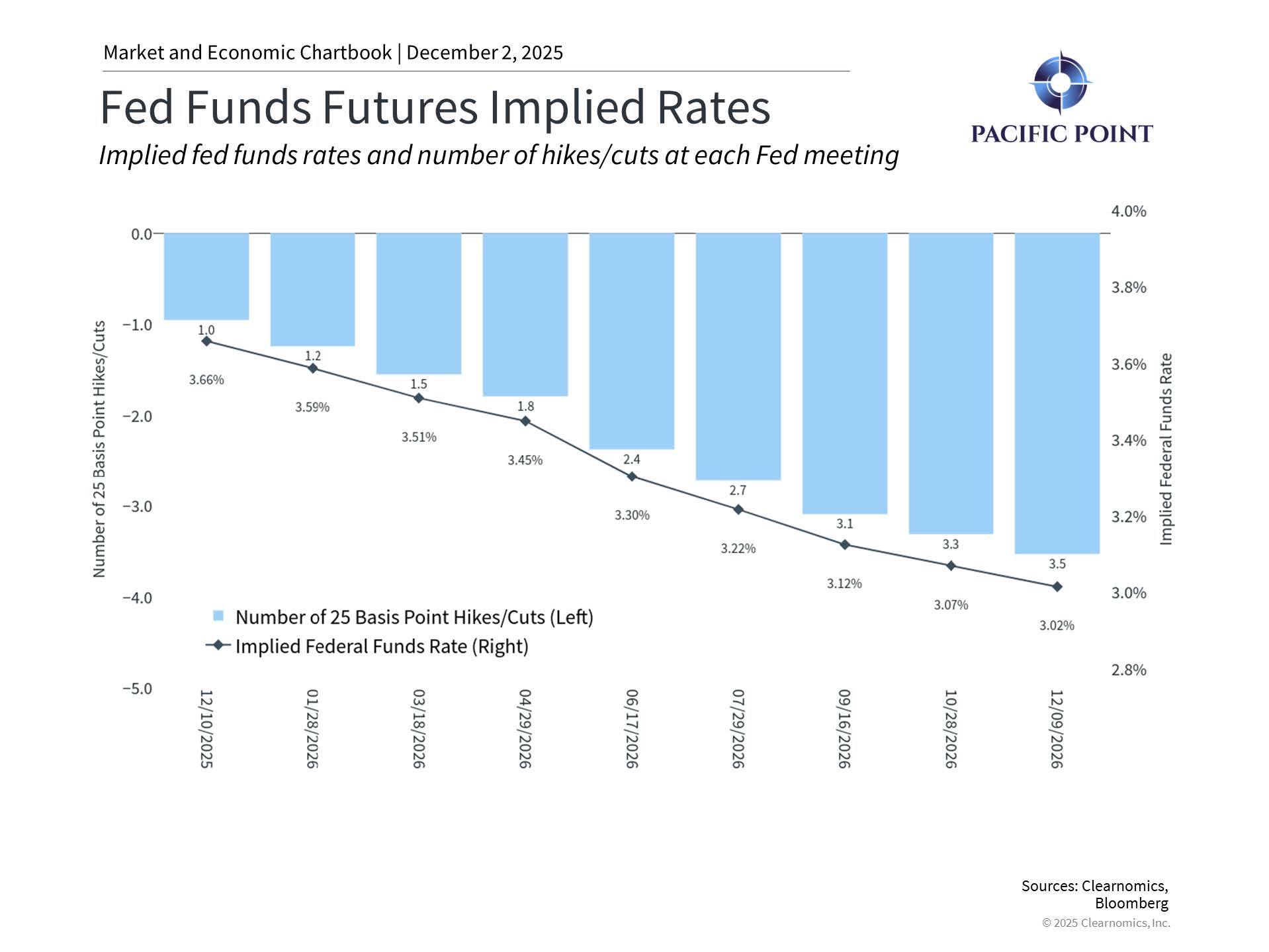

Federal Reserve rate cut expectations have evolved

These data gaps mean the Federal Reserve will approach its mid-December meeting

with incomplete economic information. Market expectations for a rate reduction at

the upcoming meeting fluctuated significantly, with probabilities declining in

mid-November before rising again. Current market-based indicators suggest the Fed

will lower rates in December, followed by additional cuts in April or June 2026.

Other economic indicators, including consumer confidence measures, have also deteriorated. The University of Michigan’s Index of Consumer Sentiment preliminary reading fell from 53.6 to 50.3 in November. This decline reflects ongoing worries among Americans regarding employment stability, elevated prices, and general financial wellbeing. Despite households feeling financial pressure, weak sentiment in recent years has not resulted in reduced consumer spending or corporate revenue declines.

THE BOTTOM LINE?

Market fluctuations in November and persistent economic uncertainty serve as reminders that stock market volatility is a normal occurrence. Investors should maintain perspective on their long-term objectives as the year draws to a close.

Clearnomics Disclaimer

Copyright (c) 2025 Clearnomics, Inc. All rights reserved. The information contained herein has been obtained from sources believed to be reliable, but is not necessarily complete and its

accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and the other information provided are subject to change without notice. All reports posted on or via www.clearnomics.com or any affiliated websites, applications, or services are issued without regard to the specific investment objectives, financial situation, or particular needs of any specific recipient and are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past performance is not necessarily a guide to future results. Company fundamentals and earnings may be mentioned occasionally, but should not be construed as a recommendation to buy, sell, or hold the company’s stock. Predictions, forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any security–including mutual funds, futures contracts, and exchange traded funds, or any similar instruments. The text, images, and other materials contained or displayed in this report are proprietary to Clearnomics, Inc. and constitute valuable intellectual property. All unauthorized reproduction or other use of material from Clearnomics, Inc. shall be deemed willful infringement(s) of this copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. Clearnomics, Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Clearnomics, Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.